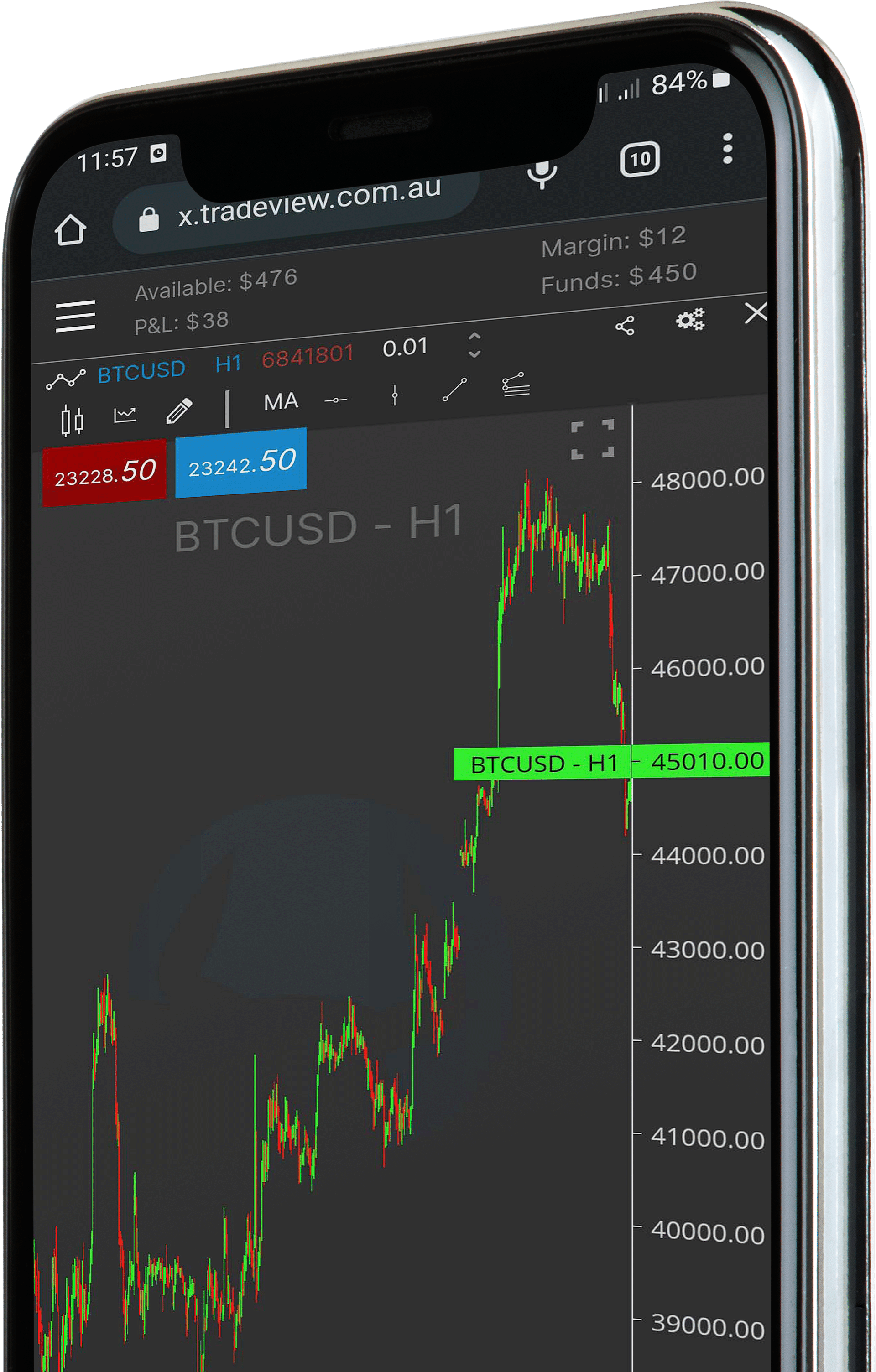

In Episode 406 of Trading Talk, we continue developing our trade management framework by introducing a breakout-based entry model and testing its performance through structured backtesting.

The focus of this session is not on predicting targets, but on managing trades dynamically. By removing fixed take-profit levels, the system is designed to stay aligned with market structure and hold strong trends for longer when conditions allow.

What This Episode Covers

- Adding a breakout entry into an existing trade management system

- Testing breakout logic using historical market data

- Managing exits without fixed profit targets

- How small logic changes can materially impact execution quality

- Improving trend participation through adaptive trade management

Why Trade Management Matters in Breakout Systems

Breakout strategies often succeed or fail based on how trades are managed after entry. This episode demonstrates how structured exit logic can reduce premature exits while still controlling risk, allowing the system to remain engaged during sustained market moves.

Rather than focusing on isolated trades, the approach shown here reinforces the importance of consistency, repeatability, and system behaviour across many trades.